Summary: The Foreign Contribution (Regulation) Amendment Bill 2026 proposes significant changes to the Foreign Contribution (Regulation) Act, 2010, most notably replacing Section 15 with a new Chapter IIIA. This establishes a Designated Authority in which all foreign contribution and assets of an organisation vest upon cancellation, surrender or cessation of its FCRA registration. During provisional vesting, the Designated Authority has the power to take possession of assets and manage the organisation’s activities, including using its foreign contribution. If the organisation fails to obtain fresh registration or renewal within the prescribed time, its assets permanently vest in the Designated Authority and may be disposed of through prescribed modes. The Designated Authority enjoys extensive powers under the 2026 Bill, and judicial intervention is largely restricted. The amendments carry serious implications for FCRA-registered organisations, demanding rigorous compliance, meticulous accounting and proactive governance.

The Foreign Contribution (Regulation) Amendment Bill, 2026 (“2026 Bill”), recently introduced in the Lok Sabha, contemplates substantial changes to the Foreign Contribution (Regulation) Act, 2010 (“FCRA” or “2010 Act”), including the introduction of a new procedure for the vesting of an organisation’s assets in a newly created Designated Authority (the “Authority”) upon cancellation, surrender or cessation of its registration under the 2010 Act.

The 2010 Act primarily applies to non-governmental organisations undertaking a definite cultural, economic, educational, religious or social programme on a not-for-profit basis. It regulates the acceptance and utilisation of foreign contribution to ensure that such inflows do not adversely affect national interest, public order or national security. Currently, around 16,000 associations are registered under the 2010 Act, collectively receiving about INR 22,000 crore in foreign contribution annually[1].

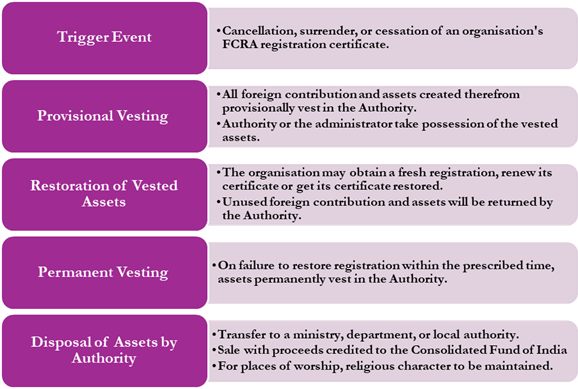

The single most consequential change introduced by the 2026 Bill is the deletion of Section 15 of the 2010 Act and the insertion of Chapter IIIA in its place to provide for vesting of assets in the Authority. Section 15 provided for the vesting of assets in “such authority as may be prescribed” upon cancellation or surrender of an organisation’s registration. Notably, no specific authority had been notified under this provision, nor had any mechanism been prescribed for the vesting and disposal of assets. The new Chapter IIIA establishes a comprehensive framework for the vesting, supervision, management and disposal of foreign contribution and assets in the Authority, defined as such officer or authority as may be notified by the Central Government. The 2026 Bill also introduces the concept of an ‘administrator’, who may be appointed to assist the Authority in the discharge of these functions. The process of vesting and the powers of the Authority are summarised in the table below.

Section 16A, as sought to be inserted by the 2026 Bill, provides that all foreign contribution and assets created therefrom shall provisionally vest in the Authority from the date of cancellation, surrender or cessation of an organisation’s FCRA certificate. The Bill also clarifies that an organisation’s registration certificate will be deemed to have ceased on the expiry of its validity period if renewal has not been applied for, if renewal has been refused by the Central Government, or if the certificate is not renewed before the expiry of its validity period. This broad provision for deemed cessation means that if any one of the specified conditions is met, it would lead to cessation of the registration certificate, making that organisation’s assets liable to be provisionally vested in the Authority.

During the provisional vesting period, the Authority or an administrator appointed under the FCRA is entitled to take possession of the vested assets and assume management of the organisation’s activities, including the utilisation of its foreign contribution for managing such assets and activities. The organisation may, within such time as may be prescribed, obtain a fresh registration certificate, renew its certificate or get its certificate restored in accordance with the FCRA, and thereafter seek the return of its assets from the Authority. Failing this, the provisionally held foreign contribution and assets shall permanently vest in the Authority. Notably, assets created or acquired partly from foreign contribution and partly from other sources are also subject to vesting, unless it can be demonstrated that a distinct or ascertainable portion of the asset was created or acquired from sources other than foreign contribution.

The Authority is required to apply the permanently vested assets and the associated foreign contribution for public purposes through one of the three prescribed modes: (i) transferring them to a ministry, department or local authority; (ii) selling them and crediting the proceeds to the Consolidated Fund of India; or (iii) where the asset is a place of worship, ensuring that its religious character is maintained and entrusting its management or operation to such person as may be prescribed. The 2026 Bill specifically provides that no key functionary of the organisation whose assets are being disposed of shall, directly or indirectly, acquire any interest in it. Accordingly, once assets permanently vest in the Authority, neither the organisation nor its key functionaries may reclaim them at the time of disposal by the Authority.

The Authority and the administrator have also been granted extensive powers for the discharge of their functions. They possess the powers of a civil court in respect of summoning and examining persons and receiving evidence, and all government officers are required to render assistance in the exercise of their duties. Additionally, any property vested in the Authority may not be transferred by way of attachment, seizure or sale pursuant to any order of a civil court or tribunal, except in accordance with the provisions of the FCRA, essentially negating the scope for judicial intervention prior to an order being passed by the Authority. Once an order is passed by the Authority, the organisation or its key functionaries may seek to have the Authority revise its order or prefer an appeal before a judge within ninety days of the order. However, the 2026 Bill does not provide any timeline within which the Authority itself must pass the initial order in relation to vested assets, thereby leading to uncertainty for organisations whose fates hang in the balance.

The changes proposed in the 2026 Bill represent a drastic shift in how the government views FCRA-registered organisations and the foreign contribution and assets held by them. Under the new law, whenever the 2026 Bill is passed and notified, the government would have an interest in organisations’ assets from the moment of cancellation, surrender or cessation of their FCRA registration. While the intent of the 2026 Bill may be to promote greater accountability and follow the trend of tightening the FCRA regime over the past few years, it risks having grave impacts on bona fide organisations that have not been able to comply on account of procedural delays or inadvertent non-compliance rather than deliberate FCRA violations. For all stakeholders and key functionaries on the organisational side, the practical implications are clear and immediate — foreign donors must rigorously evaluate compliance of Indian partners under the FCRA regime; organisations must accord registration renewal the highest priority; foreign contribution must be accounted for in meticulous detail to distinguish between assets funded from foreign and other sources; and internal governance structures must be reviewed to ensure that key functionaries are fully apprised of their enhanced duties and potential liability under the proposed amendments, as discussed further in Part II of this blog.

[1] Statement of objects and reasons of the Foreign Contribution (Regulation) Amendment Bill, 2026