Summary: The Foreign Contribution (Regulation) Amendment Bill 2026 proposes significant amendments to the Foreign Contribution (Regulation) Act, 2010, tightening the regulatory framework for foreign contributions in India. It limits timelines for receipt and utilisation of foreign contribution under the prior permission route, codifying the restrictions that began with government circulars issued in 2025. The Bill also defines the term “key functionaries,” to cover all leadership positions irrespective of organisational structure, exposes key functionaries to personal liability for organisational offences, and imposes on them a statutory duty to report an organisation’s cessation or defunct status. The evolving FCRA landscape requires organisations to review governance structures, identify key functionaries, ensure timely renewals, and maintain complete records to ensure continuing compliance.

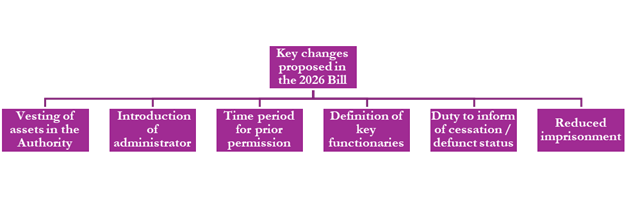

The Foreign Contribution (Regulation) Amendment Bill, 2026 (“2026 Bill”), recently introduced in the Lok Sabha, contemplates substantial changes to the Foreign Contribution (Regulation) Act, 2010 (“FCRA” or “2010 Act”). The FCRA regulates the acceptance and utilisation of foreign contribution by non-governmental organisations, with the aim of ensuring that such inflows do not adversely affect national interest, public order, or national security. Part I of this blog discussed the changes in relation to the introduction of a new procedure for the vesting of an organisation’s foreign contribution and assets in the Designated Authority (“Authority”) and the powers of the Authority in relation to the disposal of such assets. Part II highlights the other changes proposed by the 2026 Bill and the increased compliance requirements that organisations may face.

The 2026 Bill introduces greater specificity regarding prior permission for receiving foreign contribution. Under the proposed amendments, such prior permissions would be valid only for a specific project or a specified amount of foreign contribution, and the funds must be received and utilised within a prescribed period. The shift towards limiting utilisation timelines began in April 2025,[1] when the government issued circulars restricting the validity period for receiving foreign funding to three years from the date of approval and the utilisation period to four years from that date. This marked a departure from the original position under the 2010 Act, which did not impose any time limit on utilisation and permitted prior permission to remain valid for the duration of the project, accommodating longer-term and larger-scale initiatives. The 2026 Bill now seeks to codify the powers of the government to prescribe time periods for using funds received under the prior permission route, upon expiry of which such permission would lapse.

The 2026 Bill also introduces the term “key functionaries”, defined to include the directors, partners, trustees, karta, office bearers, members of governing bodies, and similar persons associated with the organisation. This broad definition encompasses all leadership positions in an organisation, making every office bearer liable under the FCRA for compliance and accountable in cases of default. A significant compliance obligation arises for organisations that cease to exist or become defunct: their last key functionaries are now under a statutory duty to inform the Central Government of the cessation or defunct status of the organisation, upon which its foreign contribution and related assets shall stand permanently vested in the Authority. All organisations and their key functionaries must be aware of this new obligation and structure their internal governance accordingly.

Further, under the proposed amendment to Section 39 of the 2010 Act, all key functionaries may also be held liable for any offence committed by an organisation, unless they can demonstrate that it was committed without their knowledge or that they had exercised all due diligence to prevent its commission. The 2026 Bill has, however, reduced the maximum period of imprisonment under the FCRA from five years to one year, along with a fine. It has also introduced a safeguard by requiring prior Central Government approval before initiating investigations into offences under the FCRA. While this measure could insulate bona fide organisations from vexatious or premature investigations, it also raises concerns regarding the scope for executive discretion in the absence of clear guidelines governing the grant or refusal of such approval to investigate.

The 2026 Bill signals a marked tightening of the regulatory environment governing foreign contributions in India, and organisations and foreign donors must start taking steps to adapt to the changing landscape. The proposed amendments narrow the scope of prior permission by imposing prescribed time limits for receipt and utilisation; extend personal exposure and liability to key functionaries for organisational offences through the introduction of a broad definition that encompasses directors, trustees, and office bearers within the compliance framework; and impose a statutory obligation on the last key functionaries to report the cessation or defunct status of an organisation. While the maximum term of imprisonment is sought to be reduced to one year, the additional requirement of obtaining Central Government approval before initiating investigations adds another layer of oversight. Overall, the thrust of the 2026 Bill is one of heightened scrutiny and accountability, in keeping with the changes to the FCRA regime over the past few years. Organisations registered under the FCRA and their foreign donors should review their governance structures, clearly identify “key functionaries” with a clear evaluation of personal exposure and liability, ensure timely renewal of registrations, and maintain rigorous records of activities and assets to ensure compliance with the evolving FCRA landscape.

[1] Further information regarding the April 2025 changes can be accessed at ‘Between scrutiny and support: Navigating recent FCRA amendments’.